Prelim Feasibility - Whitianga Block

20Ha live zoned residential development block

22 min read

Executive Summary

20 Wells Place is a large-scale residential development site in the heart of Whitianga. Comprising two adjoining freehold titles totalling approximately 216,940m2, the property is zoned for residential use and features flat, easily developable terrain, making it highly suitable for subdivision. It is the largest residential development block in Whitianga and one of only a few potential large scale greenfields projects in the district.

Strategically located close to town amenities and essential infrastructure, the site is ideally positioned to capitalise on the increasing housing demand in the Coromandel region. The property benefits from existing services in the area and excellent connectivity to the Whitianga town centre and surrounding lifestyle attractions.

With a capital value of NZD $14.6 million (July 2023), this greenfield site presents an exceptional opportunity for developers, investors, or consortiums looking to deliver a high-quality residential community in one of New Zealand’s most desirable coastal growth areas.

Site Overview

Address: 20 Wells Place, Whitianga, Thames-Coromandel District

Total Area: 216,940m2

Titles: Two separate titles (42,440m2 & 174,500m2) referred here as “4Ha block” and “17Ha block”

Zoning: Residential

Current Use: Rural farmland

Improvements: None

Legal Considerations: Utilities and drainage easements

Capital Value (as of July 2023): NZD $14.6 million (note this includes 117 Hectares total due to adjoining rural block not for sale) Lots listed in this $14.6M are Pt Arerowhero DP 19115, Lot 2 DPS 26491, Lot 2 DPS 4046, Pt Weiti 1 Blk, Lot 2 DPS 46745

Land Value: NZD $13.65 million (Includes 117 Hectare block)

Improvement Value: NZD $950,000 (existing farmhouse)

Rates: TCDC 2024/2025 $22,400 (all lots)

Site Characteristics

Topography & Contour

Flat, easy contour but low-lying coastal land. Minimal sloping/flow paths

Photos suggest there are large farm drainage channels to the North/East of the 17Ha block

Photos suggest there are coastal wetland swampy areas to the northern boundary. The northern third of the 17Ha block appears to be poor draining/potentially boggy.

The remainder of the 17Ha block to the south and the 4Ha block appear to be well drained.

The rectangular and flat shape on the edge of established housing would generally be well suited to urban expansion of the same nature nearby.

Roading and Access

The property's flat contour simplifies road construction. The potential for multiple access point on both blocks enhances traffic flow and connectivity within the subdivision. It also allows flexibility in the staging of the project with many different initial stage locations possible.

Water Supply

The blocks are within the Whitianga Water Supply areas of service. There is a 150mm PVC water main which cuts through the northern half of the 17Ha block. For a development <400 houses, this may be sufficient capacity without upgrading to trunk size water mains. As the site is flat, demand is residential and the network will be looped, it is likely the 150mm main is sufficient. Pressure checks and further design investigation would be warranted given the size of the development to determine 200-300mm upgrades are not required (significant cost). Coupled with WW and road access nearby, this would support a plan to begin initial stages down this end of the site. As staging progresses, rider mains can be installed to further service future stages.

Wastewater

The blocks are within the Whitianga Wastewater areas of service. There are WW lines bordering the site in many locations, however these are all 150mm gravity sewers. For a likely load from ~250 dwellings it will be required to complete a ~150m trunk extension up Pacific Coast Highway (300mm) to service the site from the southern boundary of 17Ha Block. An additional 550m is required to reach the initial staging point mentioned in water supply above. Likely cost for a total ~720m of gravity sewer would be $800k-$1.2M. There may be some cost sharing opportunity from Council if this benefits other Developers (unlikely looking at the nearby zoning/titling info).

Drainage

Stormwater management on this site is achievable. The open channel drain on the eastern boundary of 17Ha Block and 4Ha Block will collect gravity main flows from the development. This will service the majority of the area from the initial staging area. It is likely that retention wetlands would be developed on the far northern area of the site to provide earthworks fill and improve water runoff quality. These wetlands would serve as the outfall to the north of the initial staging area. The cost to construct the wetlands could be in the vicinity of $1M for a development of this size. The wetlands can be staged but a lot of the cost is likely to be borne at the front end of the project (prior to road sealing). There would be a number of further investigations in the planning stage to clarify the exact SW options (site topo, geotech, hydrogeological studies, stormwater modelling, ecological assessment, construction staging considerations).

Electricity and Telecommunications:

The ~20-hectare site will require both electrical and communications infrastructure to support residential development. Early consultation with the local electricity provider is essential to assess existing capacity and determine if upgrades or a new substation are needed. The electrical distribution network will be extended underground, with transformers and meter pillars installed to service all lots. Street lighting will be designed to meet council standards. Each lot will have individual electrical and communications connections, including meters and cabling. Communications infrastructure should include provision for fibre optic to meet modern connectivity expectations. Safety devices like switchgear and protection equipment will be installed to ensure reliable power supply. Planning for future technologies, such as EV charging and smart home systems, is recommended. Detailed design and capacity assessments should be completed early to define scope, costs, and staging requirements.

Topography, Contour & Drainage Flow Paths

The site appears to be generally flat, although the exact fall of the land is unclear from available contour data. A full topographical survey would confirm subtle level changes and allow flow paths to be accurately mapped for stormwater design. Flow paths will influence the stormwater network layout, the location and size of retention basins or wetlands, and help determine logical staging for civil works. The flat nature of the site is well-suited to a range of housing typologies, particularly standard detached and perhaps some limited medium-density dwellings, due to the relative ease of earthworks, slab construction, and service installation.

Hazards - Flooding

The site has a Waikato Region Flood Hazard overlay to the northern boundary of the 17Ha Block comprising ~2.5 Hectares. As mentioned previously, this is likely to be developed into a wetland area. While the remainder of the site does not have the overlay, there is a reasonable likelihood that the level of the site will have to be raised as there are questions around coastal inundation risks from sea level rise. Current modelling suggests for this land to become inundated in a 1% AEP (1 in 100 year flood) sea levels have to rise ~400mm.

For this land to become inundated in a 5% AEP (1 in 20 year flood) sea levels have to rise ~400-600mm. More work is being done by Council to guide policy in this area related to coastal inundation and flood risks. The bottom line is that this site has a high likelihood of requiring earthworks re-contouring to lift the minimum floor level of the site. This could entail up to 1m of fill and will likely introduce significant costs to do so.

Hazards - Geotechnical

No geotechnical hazards or risks can be inferred from desktop study at this stage. Test pits, hand augers or scala penetrometers may be undertaken if site access is granted under due diligence.

Earthworks

This site has a high likelihood of requiring earthworks re-contouring to lift minimum floor levels above future flood risk thresholds. However, only the developable portions of the site would need to be raised - areas intended for wetlands or stormwater management are expected to remain near existing levels. Assuming 4–6 hectares of the site are set aside for wetlands, the remaining 15–17 hectares may require filling. At an average of 1 metre of lift, this equates to approximately 150,000–170,000m³ of engineered fill. Depending on wetland location and excavation depth, a portion of this material could be sourced from on-site cuts (potentially around 50,000m3). Fill suitability and compaction requirements will need to be confirmed by early geotechnical investigations. Imported fill or cut-to-fill balancing within the site may be necessary.

The cost of importing, placing, and compacting fill is estimated at $30–$40/m³, while onsite cut and placement costs would be lower at around $10–$15/m³. Based on these assumptions, total bulk earthworks could cost between $3.8M and $5.15M, with a blended unit rate of ~$24–$32/m² for land requiring fill. These costs are significant and will need to be confirmed through detailed geotechnical and bulk earthworks design at the planning stage and will impact staging, platform design, and services installation. At this early stage, we would assume a per lot earthworks costs contributing $30k per lot. While this is conservative, it is unclear at preliminary feasibility the extent of flood mitigation earthworks that would be required and exactly where this material would be sourced. This is a significant risk in acquiring this site.

Soil Contamination

A desktop review has not identified any evidence of soil contamination on the site. There are no known historical land uses or activities associated with contamination risk. Nonetheless, detailed soil testing and environmental site assessments will be undertaken during the planning phase to confirm these preliminary findings. Should any unexpected contamination be identified, appropriate remediation measures will be implemented in accordance with relevant regulatory requirements.

Environmental Considerations and Significant Features

No significant environmental constraints have been identified within the site boundaries. The property does not appear to contain any sensitive ecological features or overlays that would materially impact the development. However, as part of the planning and resource consent process, standard environmental assessments will be required. These are expected to include stormwater management planning and ecological impact assessments to ensure compliance with environmental standards and to inform development design where necessary.

Overlays, Controls, Designations, and Structure Plans

The site is located within an existing structure plan area, which provides a framework for land use and infrastructure planning. There are no additional zoning overlays, designations, or environmental controls that are expected to impose significant constraints on development. This is anticipated to support a relatively streamlined consenting process.

Heritage, Archaeology, and Sites of Significance

A desktop review of heritage and archaeological records has not identified any sites of significance within the property. No field-based assessments or surveys have been conducted to date. While no issues are currently anticipated, further investigation may be required during the planning phase to confirm these findings and ensure compliance with heritage and archaeological requirements should any items of interest be discovered.

Development Potential

Market/Suburb Analysis

Situated in a rapidly growing coastal town, this block enjoys a prime location near both the Whitianga town centre and the beach, providing easy access to essential amenities and desirable lifestyle attractions. The area is experiencing steady population growth, which continues to drive demand for residential housing and support broader community development.

Recent market data indicates a stabilising but improving post Covid property market. While overall conditions remain moderate, short term key indicators are trending positively: median days to sale are decreasing, and sales volumes have increased over the last quarter. As a result, median sales prices have begun to rise. Over the longer term, Whitianga has shown consistent growth in demand, driven in part by post-pandemic lifestyle shifts, with many seeking a higher quality of life outside the main urban centres. Given the lengthy development timeframe of this bulk land purchase, long term demand trends de-risk this project to some extent as revenue escalation profiles are likely to stay positive and likely higher than the national average.

Net Developable Area (NDA)

Given the flat terrain and residential zoning, a significant portion of the 21.6 hectares is likely developable. Assuming standard allowances for roads, green spaces, and infrastructure, as well as conservative estimates of wetland sizing an estimated 14.5 hectares could be developed into housing. This is dependent on topography and the treatment of potential low-lying areas with on-site fill as well as appropriate sizing of wetlands. The NDA would be further optimised through additional rounds of feasibility as additional engineering inputs such as topo surveys, flood modelling and infrastructure constraints become available.

Net Site Yield

Based on typical lot sizes ranging from 500m² to 800m²:

Estimated Lots: Approximately 190 to 250 residential lots. As an early-stage simplification, this excludes the effect of some likely superlots and small pockets of higher density which the Council may encourage for a diverse product mix. Estimated yield would likely be closer to 600m2 with the most likely scenario an NDA of 14Ha with 600m2 average lot size and ~230 lots. Further discussion with Council on policy direction in this area would increase the accuracy of Site Yield predictions.

Lot Size Variability: Potential for a mix of lot sizes to cater to diverse market segments as well as improving sales absorption rates throughout the extended development and de-risking the project.

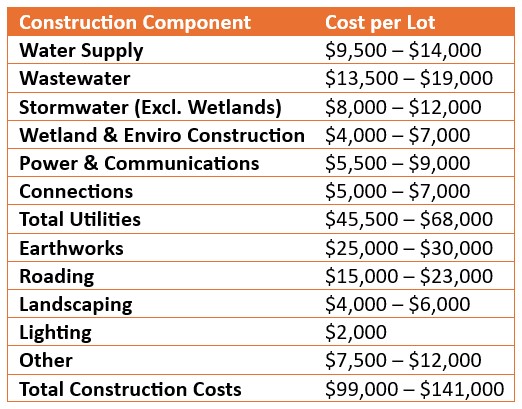

Estimated Cost Breakdowns

Based on the above considerations, early-stage feasibility gives the following initial benchmarks for costs per lot. These are based not on actual IFC priced plans but likely ranges from assessment of the sites specific characteristics. These factor in both the fixed cost components (eg. of utilities upgrades to service the site to the starting stage area) as well as the likely variable costs (eg. costs in relation to lots created).

Further rounds of feasibility and engineering assessment would reduce the variability cost per lot but for a first cut exercise the mid-point $120k per lot would be a reasonable starting point to guide the initial estimate of RLV. Adjustments to this can be made based on preliminary design and actual net site yields. Construction contingencies are in addition to these figures.

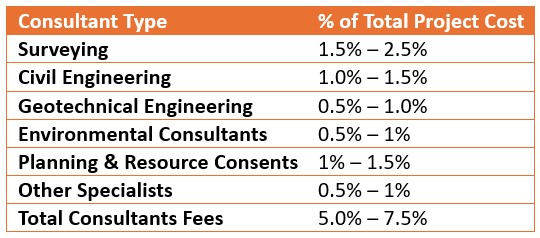

Variation in Surveying costs would be guided by local operators and their scope of services on offer. Professional fees allocations around 5.5% is a reasonable number to take forward at this stage. Development Management and Construction Supervision fees are in addition to Consultants fees above.

Statutory Fees

1.5% to 2.5% of total project cost. This accounts for Council Processing Fees, Engineering Plan Approvals, Subdivision Consent, Building Consents (if applicable), LINZ & title lodgement.

Development Contributions $19.8k per lot for Whitianga.

Given the current trend in NZ Local Government costs, escalations at minimum 7% per annum should be applied to all statutory fees.

Contingencies

Contingencies are closely aligned with the assessment of project risks. An incorrect understanding of those risks - or the inappropriate selection of contingency rates can lead to significant errors in development feasibility and valuation. This equates to missing out on opportunities or locking in mis-priced deals.

For this project, we have applied a Construction Contingency of 18% to account for uncertainties in civils costs, and an overarching Project Contingency of 12% to reflect broader development risks such as planning, infrastructure, market, and delivery timing exposures.

These contingency allowances are exclusive of any cost escalations, development margins, or abnormal cost allowances already captured. The contingencies will be refined progressively as further engineering inputs, geotechnical data, and design development become available.

Land Holding Costs

Land holding costs include expenses incurred during the ownership phase prior to and including construction commencement. These typically consist of:

Council rates

Property insurance

Security and basic site maintenance

Any costs associated with finished, unsold lots

Interest costs (if debt-funded, not applicable here)

These costs have been applied on a pro-rata monthly basis over the projected holding period in line with the anticipated development staging and cash flow profile. Allowances will be updated as more accurate project timelines and funding strategies are confirmed.

Selling Costs

Selling costs for the development include all expenses directly associated with the marketing and sale of individual lots or dwellings. These typically comprise:

Bulk agent sales commissions 2% of gross sale price (subject to local market norms and sales strategy)

Marketing and advertising-including signage, digital campaigns, staging, brochures, and promotional events

Legal fees- for preparation of sale & purchase agreements and settlement documentation

Settlement costs - including conveyancing disbursements and coordination

Sales office costs

Incentives/rebates - offered to buyers (excluded here)

These costs are typically applied as a percentage of revenue - we have assumed a blended total selling cost allowance of 3.5% of gross sales revenue for this feasibility. This will be refined as the sales strategy is developed and agency terms are confirmed.

Finance Costs

Finance costs for large-scale developments typically include all expenses related to securing and servicing debt during the life of the project. These costs can be significant and are influenced by the project staging, timing of cash flows, and risk profile.

Key finance cost components include:

Loan interest - applied to drawn-down amounts over time; calculated based on the projected cash flow and drawdown schedule

Establishment fees - upfront costs charged by the lender for setting up the facility

Line fees (undrawn commitment fees) - applied to the undrawn portion of the loan facility, charged monthly or quarterly

Brokerage or advisory fees - if finance is arranged through an intermediary

Legal and documentation costs - for loan agreements, securities, and compliance

Valuation and due diligence fees - often required by lenders during facility approval

In this preliminary feasibility assessment, finance costs have been excluded for simplicity. This allows for a clear evaluation of Project IRR based solely on the development’s unleveraged cash flows.

Depending on acquisition structuring and client-specific objectives, a detailed financing strategy would be introduced in future iterations. This would include optimisation of equity and debt sizing, timing of drawdowns, interest costs, and associated fees - all aimed at maximising Equity IRR and aligning with target return thresholds. A full financing model can be integrated once lender engagement begins or capital structuring preferences are confirmed.

Professional Fees

Revenue for future lot sales are escalated at the following compounded rates to account for changing market conditions

Revenue Escalations

Costs categories are escalated at the following compounded rates to account for changing market conditions

Cost Escalations

Timeframes & Staging

Planning & Approvals

Anticipated 12–18 months for subdivision consenting, detailed engineering approvals, and resolution of flood modelling/earthworks strategy.

Early engagement with Council on wastewater/water servicing and stormwater discharge required to avoid downstream delays.

Potential parallel processing of civil engineering design and consent conditions to compress programme.

Earthworks & Servicing

Stage 1 earthworks (flood fill, roading spine, bulk services) expected to take ~12 months, sequenced outside peak rainfall seasons.

Bulk infrastructure (stormwater ponds, pump station upgrades, network connections) delivered upfront, enabling subsequent stages to connect with minimal duplication.

Subdivision Staging

Project lends itself to 3-4 stages, each yielding ~50-70 lots.

Stage 1 focuses on higher-ground land (lower fill requirement) to generate early revenue and proof of market absorption.

Later stages release progressively more lots, aligned with demand, capital availability, and infrastructure milestones.

Overall Programme

First titles achievable Year 3, subject to early planning momentum.

Project can be delivered over 8-9 years in base case, with flexibility to accelerate or slow depending on market absorption and funder requirements.

Staged approach smooths cashflow exposure and reduces market-cycle risk, while maintaining optionality for partial sell-down to other builders/developers.

Product Mix & Sales

Target Market Segments

Local demand: families and permanent residents seeking larger, traditional sections with space for sheds, boats, and outdoor living.

Lifestyle buyers: semi-retired couples and second-home purchasers who value larger coastal lots and proximity to amenity.

Investors: relatively minor component, as Whitianga’s market favours owner-occupiers and lifestyle-driven purchasers.

Product Typologies

Detached homesites (70–75% of yield): 500–650 m² sections forming the bulk of supply, suited to mid spec family dwellings.

Lifestyle / premium frontages (15–20% of yield): 700–900 m² sections oriented to open space, waterways, or view corridors, capturing lifestyle buyers and higher margins.

Compact lots / duplex (5–10% of yield): 400–500 m² sites included sparingly to broaden affordability and meet Council diversity expectations, but not driving average lot size down materially.

Blended across all stages, the mix delivers an average of ~600 m² per lot, consistent with Whitianga’s existing market preference and lifestyle positioning.

Pricing & Sales Rates

Vacant Lot Pricing

Standard detached (500-650 m²): $450k-$525k

Premium / lifestyle lots (700-900 m² with frontage, open space, or views): $525k-$600k+

Compact (400-500 m², limited allocation): $400k-$450k

Blended average across the estate: ~ $500k per lot

Market Positioning

Pricing reflects Whitianga’s scarcity of serviced, zoned land and sustained demand for larger lifestyle-oriented sections.

Benchmarking against recent sales shows strong buyer willingness to pay a premium for larger sites with flexibility for sheds, boats, and coastal living setups.

Sales Absorption

Forecast 35-45 lots sold per annum, balancing steady demand with buyer capacity at $500k average.

Absorption likely strongest in early stages where pent-up demand exists, with later premium releases staged to maximise value uplift.

Pre-sales campaigns, staged release strategies, and builder-aligned packages can be used to accelerate uptake if required.

Feasibility Modelling

Risk Assessment & Project Hurdle Rates

The target internal rate of return (IRR) for this project has been set at 23%, reflecting the extended delivery timeframe, staging complexity, and regional market dynamics inherent in this large-scale greenfield development. Given the 10-15 year horizon and the multi-staged nature of the site, a higher risk-adjusted return is required to offset potential uncertainties in construction costs, planning approvals, infrastructure delivery, and market absorption. While the project is located in a regional growth area with strong long-term demand fundamentals and a high-quality site, the scale and duration introduce material holding, potential funding, and exit risks. Accordingly, the IRR hurdle has been calibrated to reflect these strategic and financial considerations, ensuring alignment with typical industry benchmarks for long-duration residential land development in non-metropolitan markets.

Acquisition Price

The initial acquisition price for feasibility modelling was $10.0M (excluding GST). This is used only as an iterative number only to give visibility on how returns would look at this level under all previous feasibility assumptions. Settlement terms on the land acquisition price were assumed at 10% deposit upfront in Month 0, followed by the remaining 90% payment in Month 2. The Summary of Financials section below, has further information on calculated residual land values under Scenario 1 & 2.

Note that the residual land value can be altered by amending the settlement terms eg. Multiple payments over multiple years. Based on preliminary negotiations with the Agent, this could be an option if Vendor price expectations are higher than any initial offer.

Feasibility Modelling - Scenarios Input 1

Some key assumptions for the Scenario 1 development of 15 Hectares NDA are as follows:

Average lot sizes of 600m2 with a mix of lot sizes between 450-800m2 and a small amount of superlots and higher density sites outside this range.

No houses to be developed, lots sold as lifestyle lots

Average lot sale price of $510k inc GST (present value)

Pre-construction period of 18 months.

Civil construction period of 12 months per stage

Multi-staged development, split into 4 stages of civil construction

Civil construction stage start dates; Month 18, 48, 78, 108

Statutory fees and development contributions in line with current 2025 rates

Construction Contingency of 18% to account for uncertainties in civils costs, and an overarching Project Contingency of 12%

No build to rent

Project completion, May 2036

Feasibility Modelling - Scenarios Input 2

Some key assumptions for the Scenario 2 development of 13 Hectares NDA are as follows:

Average lot sizes of 600m2 with a mix of lot sizes between 450-800m2 and a small amount of superlots and higher density sites outside this range.

No houses to be developed, lots sold as lifestyle lots

Average lot sale price of $520k inc GST (present value)

Pre-construction period of 18 months.

Civil construction period of 12 months per stage

Multi-staged development, split into 4 stages of civil construction

Civil construction stage start dates; Month 18, 47, 76, 105

Statutory fees and development contributions in line with current 2025 rates

Construction Contingency of 18% to account for uncertainties in civils costs, and an overarching Project Contingency of 12%

No build to rent

Project completion, December 2035

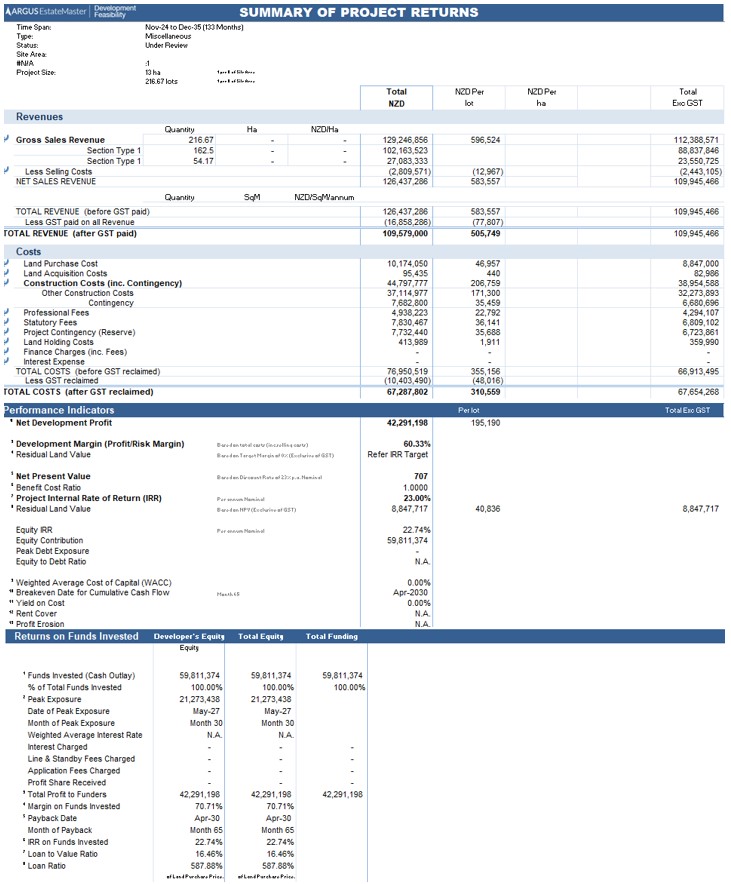

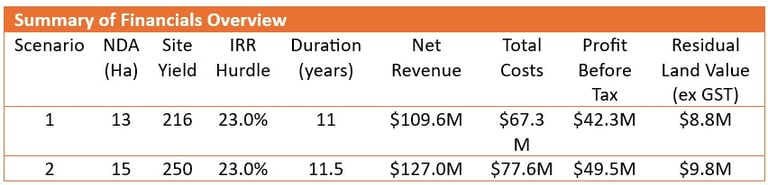

Estimated escalated sales revenue at $109.6M throughout the staged project

Estimated escalated costs at $67.3M throughout the staged project

Estimated Net Development Profit $42.3M

Peak exposure of $21.3M, with cumulative cash outlay of $59.8M

Project breaks even in April 2030

Residual Land Value assessed at $8.8M exc GST under IRR Target Hurdle of 23.0% and a 10/90% settlement agreement. This equates to land acquisition costs of $10.2M inc GST (or approximately $47/m2 for the full site).

Summary of Financials - Scenario 1

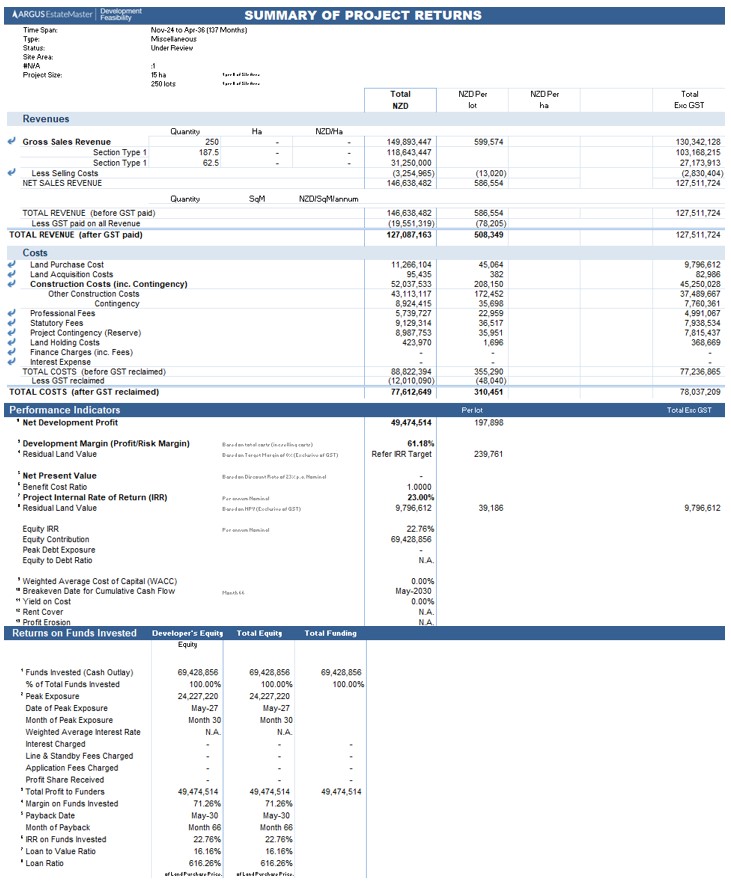

Estimated escalated sales revenue at $127.0M throughout the staged project

Estimated escalated costs at $77.6M throughout the staged project

Estimated Net Development Profit $49.5M

Peak exposure of $24.2M, with cumulative cash outlay of $69.4M

Project breaks even in May 2030

Residual Land Value assessed at $9.8M exc GST under IRR Target Hurdle of 23.0% and a 10/90% settlement agreement. This equates to land acquisition costs of $11.3M inc GST (or approximately $52/m2 for the full site).

Summary of Financials - Scenario 2

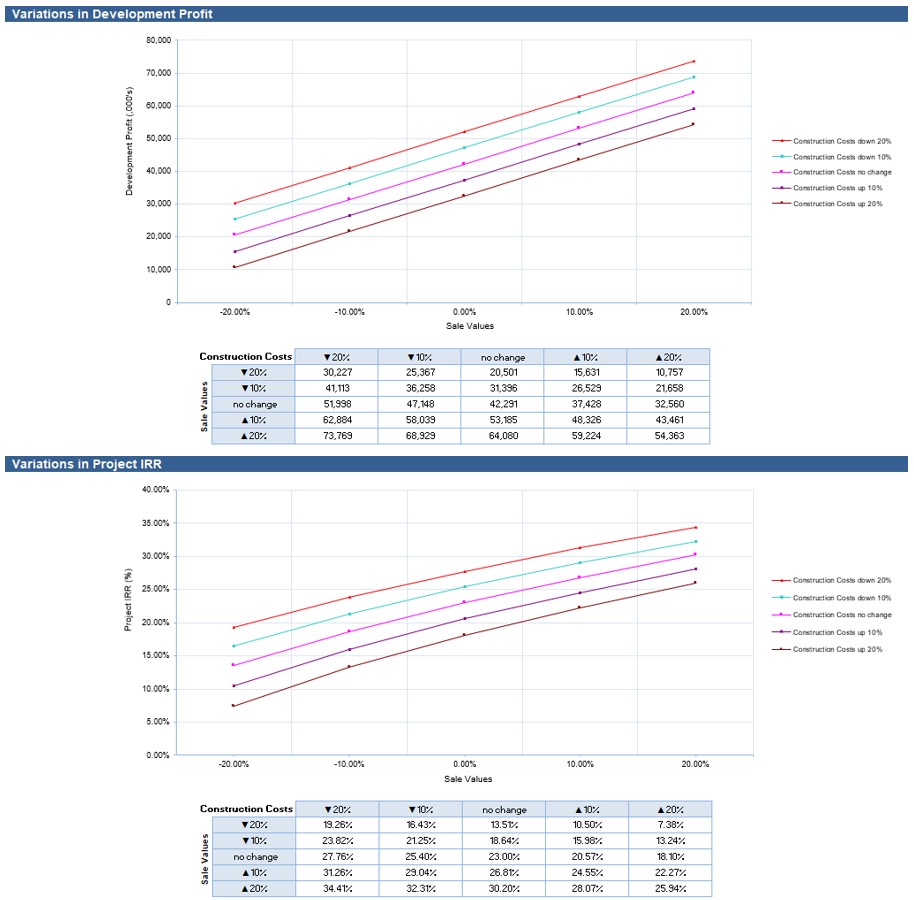

A sensitivity analysis has been undertaken to test how changes in key assumptions such as yield, land cost, or revenue impact project returns. This allows assessment of the development’s resilience under varying scenarios and helps identify thresholds where financial viability may become marginal. The results highlight how closely RLV is linked to core drivers like density and land value. Only two scenarios were explored here and they represent the likely boundary conditions for the desktop exercise ie. The upper and lower bounds. In reality, the most likely (yet still conservative) development scenario would be nearer to a midpoint site yield (~230 lots), until later stage engineering feasibility can fine tune the NDA of the site.

Sensitivity Analysis

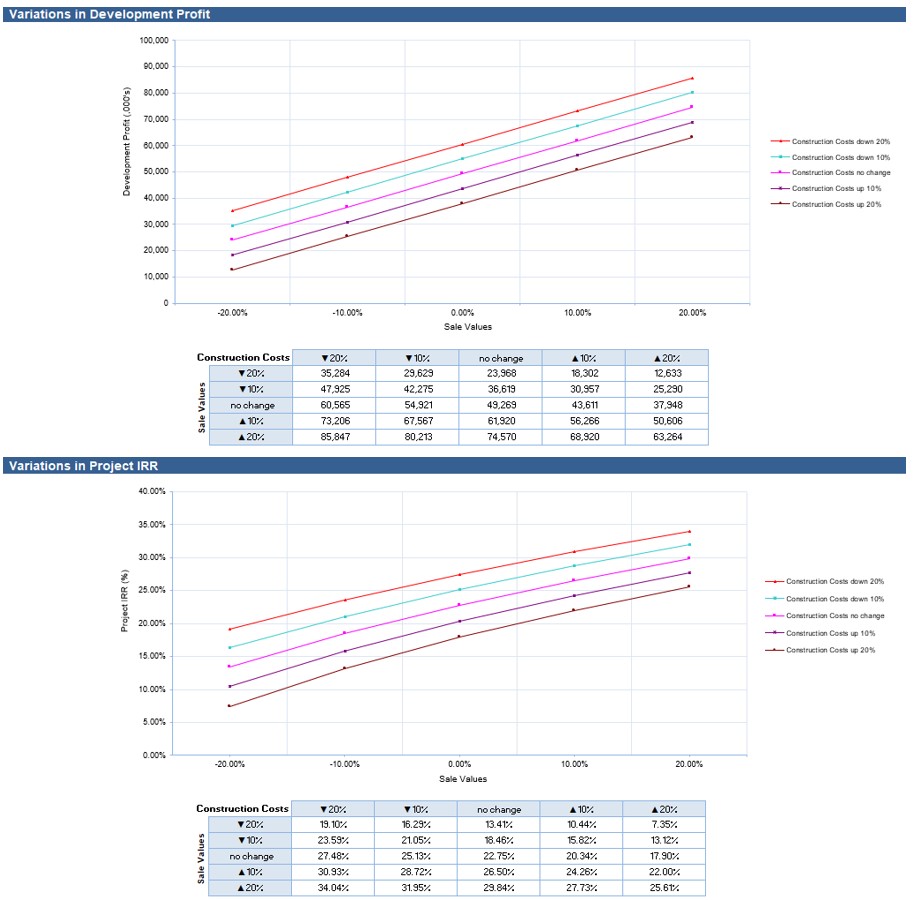

Sensitivity Analysis - Scenario 1

- Under our estimated worst-case revenue and cost scenario, this project will remain profitable

- Under our estimated worst-case revenue and cost scenario, this project will remain profitable

Sensitivity Analysis - Scenario 2

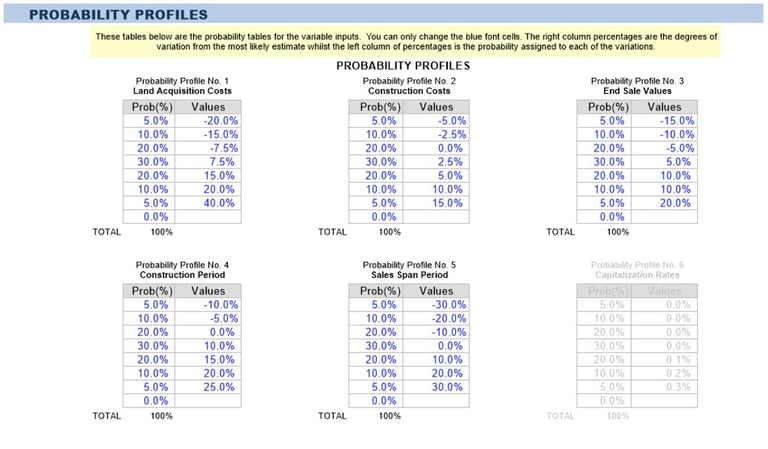

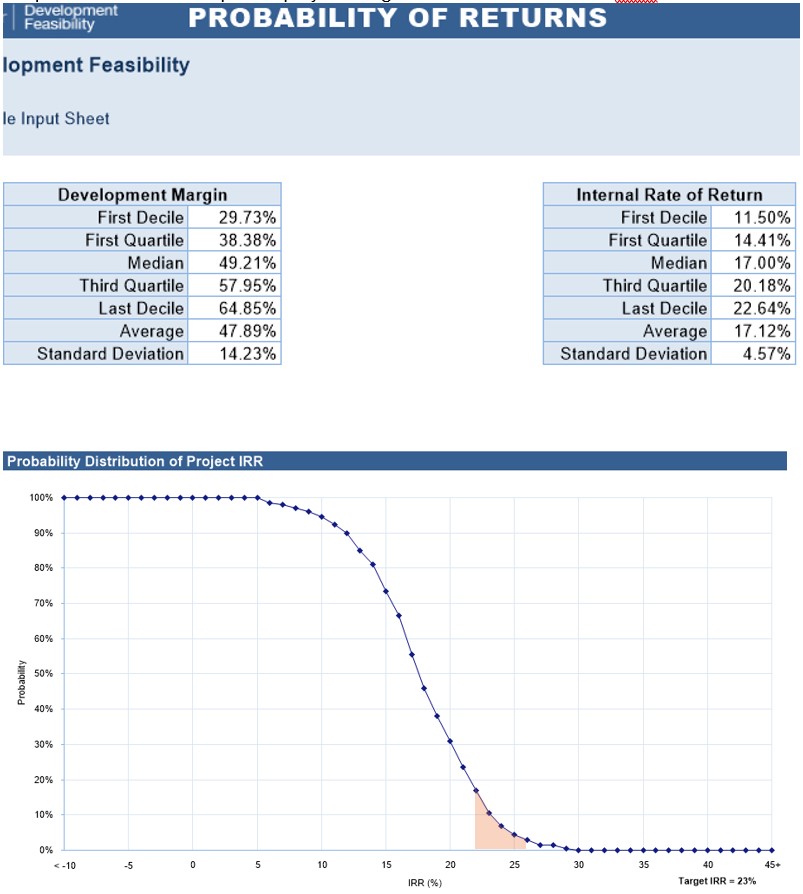

A probabilistic analysis was conducted to account for uncertainty in key project inputs such as land acquisition, construction costs, construction period, revenue and sales span periods. Rather than relying on a single-point estimate, this approach uses a range of values and assigns probabilities to different outcomes, through Monte Carlo simulation. The result is a distribution of possible financial outcomes - such as IRR and development margin, providing a more robust view of project risk and return. This helps inform decision-making by identifying the likelihood of achieving target returns and the range of downside exposure.

For this project, we applied conservative realistic probability profiles as shown below. Land acquisition cost is the most variable distribution. This reflects the fact the owners probably don’t know what the land is worth, given a lack of precedent in the area. The mid-point is based off a $10M purchase that was initially fed into the model. The upper bound of +40% is around the CV at $14M while the lower bound is at $8M. Early-stage discussions with the Agent would narrow the variance here.

The profile for construction costs and construction period are both skewed towards moderate but typical cost overruns/project delays for projects of this scale. Note that this is in addition to burning through construction contingencies for construction costs before the distribution applies. Without the contingency factor, these profiles would be estimated higher.

End sales values are skewed slightly toward optimistic sales values over the project duration. Due to the longer project durations, we have reduced the variance. It is likely over ~15 years for property prices to revert to levels near to historical CAGR. In addition, revenue escalations over the project were slightly bearish, assuming that revenue would compound generally at 5% per annum, below the historical CAGR. Nonetheless, we are of the opinion that this area will perform at or above historical CAGR over the next 15 years, given current lifestyle trends and there is likely conservatism built into the model with 5% escalation assumptions.

The profile for sales span period was taken as a neutral distribution. In our initial calculations for absorption rates and sales span periods, we benchmarked against average lot sale rates for two other similar large scale coastal developments in the area. Both projects had similar absorption rates and so we have minimised the variance of the profile here to some degree. Note that sales span periods are difficult to predict in a location such as this and can be highly dependent on choosing the right product mix as well as external factors relating to economic and lifestyle trends. Given the longer project durations likely spanning over many changes in market conditions, it is reasonable to assume fairly neutral conditions when benchmarking to other similar developments in the area.

Probabilistic Analysis

Inputs for probability profiles of key project variables

Output distributions of expected project margins. Based on 200x monte-carlo simulations

We previously assessed the risk of this project as warranting an IRR range between 22-26% with the target 23% IRR. Following probability simulations, we can see that under what we consider to be likely scenarios of project performance, there is a ~3-17% chance of hitting this target return. From the distribution graph, it can be inferred that under these conditions it is likely that this project would make a minimum 15% IRR (75% likelihood). The distribution is reflecting that under conservative assumptions, the early-stage estimates of the project are that it could be a marginal undertaking but still worth exploring. If further clarity can be made through confirming site yield efficiencies, infrastructure requirements and costs then it may be possible to de-risk the downside margins of the project. From a site acquisition perspective, this information would lead to early-stage discussions tending toward the lower end of residual land value predictions.

Conclusion

Recommendations

For those targeting shovel ready projects, it’s a site for a developer who understands the local absorption rates and how fast they can sell the lots and at what price point. There is only 2 or 3 contenders in the area that would have the prior experience and IP to understand the revenue side modelling of a long duration project such as this. Out of town developers may have interest in the site as primarily a landbank initially, with the intention to develop many years down the track. National scale developers may see value in the site from a diversification perspective, to offset a workbook of primarily urban developments. There is one NZX listed Developer that has completed projects in the area that would fit this category. Institutional funds may be a contender to purchase. With likely lower target hurdle rates, the price they could offer would potentially outbid the competitors.

Speculative Investors/landbankers may also show interest but likely not with intention to develop given the major capital requirements. Given the lack of other residential land in the area, some landbankers may be attracted by the ability to control the housing supply in the area and/or dripfeed the market in small stages. Landbankers may also be attracted by the ability to unlock some further land value through servicing the site, however given the regional nature of the site this would warrant fairly high IRR hurdle rates. It would be difficult to get a timely return, and this strategy would be better employed near larger metropolitan areas.

Strategic Considerations

Strengths

Almost full control of the residential housing supply in Whitianga, a high growth location.

Clean site, easy topography if potential flooding and drainage considerations can be addressed.

Multiple staging options, minimal constraints

Favourable infrastructure connectivity

Post pandemic, a strong market for lifestyle sections with Whitianga now supporting a greater range of employment opportunities as well as being the hub for the province.

Risks

Possibly flood prone land which may trigger larger scale earthworks and/or loss of NDA. Risk is largely accounted for, but early flood modelling and discussion with Council re their appetite for full scale development of the site should be sought.

The scale of development may trigger additional capacity constraints. To be clarified with early discussion with Council Engineers.

Not a likely contender for small drip-fed staged development due to the early-stage infrastructure sunk costs being capital intensive.

Long duration development ~11 years. Large capital requirements (peak projected cashflow exposure of $20-25M). Projected breakeven after 6.5 years. A site for larger scale developers or those with access to major financing.

Summary - Why We Like This Site

Strategic Location & Market Demand

Largest single residential-zoned landholding in Whitianga, with control over the town’s long-term housing pipeline.

Strong underlying demand driven by coastal lifestyle migration, steady population growth, and limited alternative supply.

Well-positioned relative to town centre, beaches, and regional amenities, offering enduring appeal to both local and lifestyle buyers.

Site Fundamentals

Flat, regular-shaped, and well-located block with minimal physical constraints relative to comparable greenfield projects.

Serviceable from existing water and wastewater networks with manageable upgrades, ensuring development feasibility at scale.

Flexible staging potential allows phased delivery in line with market absorption and capital availability.

Development Economics

Conservative modelling supports yields of ~216-250 lots, with a blended mid-case closer to ~230 lots.

Residual land value benchmarks $8.8M-$9.8M (ex GST), supporting competitive acquisition negotiations.

Robust profit margins ($42M-$50M across scenarios) and acceptable downside resilience demonstrated under sensitivity testing.

Probabilistic modelling shows 75%+ likelihood of achieving IRR >15% and meaningful upside potential with de-risking.

Strategic Fit

A rare opportunity for a well-capitalised developer, listed entity, or institutional fund to secure a region-defining site.

Supports both immediate staged development or longer-term landbanking, offering optionality across investment horizons.

Potential to deliver a masterplanned community that sets the benchmark for residential living in the Coromandel.

Risks & Mitigation

Flooding and fill requirements are the largest technical risks - early geotechnical and flood modelling critical to confirm costs.

Long duration and large peak cashflow exposure limit the field to experienced operators or deep capital institutions.

Council engagement on infrastructure capacity and coastal hazard policy will be a key determinant of certainty.

This is the only large-scale, zoned, developable block in Whitianga, giving effective control of local housing supply in a high-demand coastal growth market. Despite flood risk and capital intensity, the site is straightforward in planning/zoning terms, partially infrastructure-serviced, and economically feasible under conservative assumptions. It offers strong strategic value to any party seeking scale, control, and long-term upside in one of New Zealand’s most desirable lifestyle regions.