From Raw Dirt to Titled Lots

Understanding the Land Value Escalator

7/15/20256 min read

The most reliable way to add value to land is to progressively remove uncertainty. From raw rural paddocks to titled residential lots, land in NZ and Aus can increase in value by a factor of 10–100x per square metre as planning and infrastructure hurdles are cleared.

Understanding this pipeline and where land sits on it is critical to identifying profitable acquisitions, landbanking strategies, or infill development projects.

Step 1: Rural Land (No Services, No Planning Signals)

Typical value: $5–$50/m²

Use: Grazing, rural residential, or lifestyle

Development risk: Very high

This land has no zoning signal, no structure plan guidance, and no nearby infrastructure. Value is based on its existing use only. Typically targeted for long-hold speculative plays or agricultural use, not development. The North Waikato Sleepyhead acquisition of ~176 hectares of farmland for master planned residential and industrial development is a good recent example in NZ of a Developer attempting to seek bulk rural land at the lowest possible price with the intention to upzone and develop. It is likely they paid in the vicinity of $10-15/m2 for this farmland. In Australia, there are numerous examples (Stockland, Mirvac, Lendlease to name a few) where townships have been developed through major rural land deals leading to likely 100x uplift in land value from rural to titled.

Step 2: Future Urban / Identified Growth Areas

Typical value: $30–$300/m²

Use: Still rural, but within a structure plan or designated growth corridor

Development risk: High, but improving

Land may be designated “Future Urban” or earmarked for intensification under regional planning documents. While it cannot yet be developed, zoning certainty begins to price in. Buyers at this stage are typically long-term developers or syndicates. Within these zones Councils advance the infrastructure planning and layouts.

There can still be high variation of $/m2 within these zones and values move according to Developer acquisitions, infrastructure announcements or other factors such as hazard mapping. At this stage, Developers and speculators typically start to appear with the best sites being cherry picked at the early stages. Some of the sites within this zone are well poised for early development and it may be only a matter of a couple years before machnes break ground. Other sites within these zones can sit dormant for a very long time with no development ever likely in the foreseeable future. Agents have a field day with these types of properties pitching subprime land which may never develop at the same $/m2 rates as prime sites where development is imminent.

Unlike with the rural or farmland in Step 1 which you may just be able to on sell at similar rural rates, mistakes in selecting future urban land can be extremely costly. There are a litany of examples from the NZ pandemic boom where Investors were scooping up whatever they could with disregard of the fundamentals of the land they were purchasing. Many of these properties have been on the market for three years now and will likely remain so until the next major upturn.

Step 3: Live Zoned, No Services

Typical value: $100–$400/m². Infill sites, unserviced a lot higher

Use: Zoned residential or mixed-use, but not yet serviced

Development risk: Moderate

Land is now legally zoned for higher density, but lacks key services (water, sewer, drainage etc). Typically in pre-structure plan delivery stages. Value increases significantly once the zoning becomes operative, even if services are years away.

Often acquired by developers seeking to bank margin from rezoning or consent uplift.

At this stage in the process, holding costs can become significant. Councils usually impose exorbitant rates on these type of properties and not because they are collecting your recycling bins anymore often. The increased rates are a revenue collecting mechanism as well as a tool to force ownership changes from Investors to Developers. Councils don’t want people land banking and choking the supply of zoned land so they incentivise land bankers to sell.

For infill sites, typical value $/m2 for sites that are effectively unserviced (via capacity constraints or difficulties accessing nearby services) would be similar rates to that of nearby surrounding properties ($500+/m2 depending on suburb and size etc).

Step 4: Zoned and Serviced

Typical value: $100–$800/m²

Use: Ready for subdivision, development feasible

Development risk: Low–moderate

At this point, all required infrastructure is available at the boundary or nearby. Titles remain with the parent lot, but subdivision can proceed upon council consent. Sites in this category attract builder interest and may be pre-sold for margin rather than built out. At the lower end of the $/m2 spectrum would be larger scale bulk land blocks on the periphery of smaller towns that is possibly still used as farmland but otherwise ready to develop. At the higher end of the spectrum would be a small site that is clearly a prime target for quick development (often an old farm house that was historically subdivided to a smaller lot).

It's important to note that by this stage our $10/m2 rural land purchased in Step 1 is clearly worth significantly more, however major costs (and time) will likely have been absorbed to get to this point. While it may be edging closer to 100x from original purchase, in reality a good uplift would be 30% IRR, factoing in holding costs and upzone planning costs. Depending on the timing of when the land was purchased, per annum returns on the investment could be anywhere from negative to astronomical. The key here is capitalising on Council intentions, timing the market, compressing the zoning change timelines and minimising the infrastructure spend/contributions. Not your average strategy of the average property investor and typically carrying major cost, time and possibly political lobbying considerations.

Step 5: Titled Small Lots

Typical value: $500–$1,200+/m²

Use: Fully consented, titled residential land

Development risk: Low

At the end of the development pipeline lies the polished product: subdivided lots with titles issued, services connected, and dwellings ready for construction or resale. This is where value is most visible and buyers and builders compete strongly for well-located land that has already cleared the hurdles of planning, engineering, and legal compliance. Depending on the suburb, frontage, and planning controls, this is also where prices tend to reflect the full uplift from the earlier stages of transformation.

Much of the true value creation in property development happens long before the houses are even drawn on paper. The process of moving a parcel of land through planning, zoning, servicing, and subdivision can create exponential value increases per square metre, especially in undersupplied or high-growth markets. This concept is often referred to as the land value escalator.

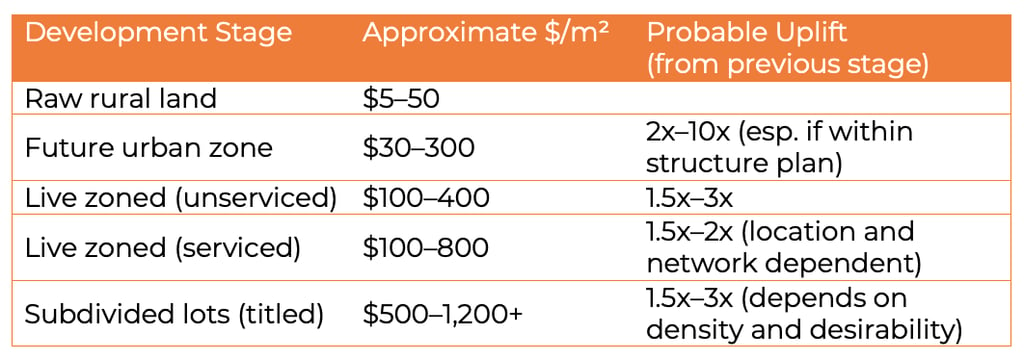

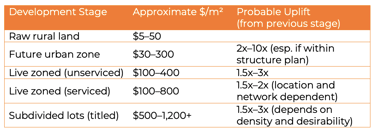

Below is a simplified table that illustrates the typical value uplift developers and landbankers can expect as land moves through each stage of the pipeline (note, this is very much location dependent):

While these numbers are broad estimates, they provide a useful framework. Uplift is highly context-sensitive and shaped by local council policies, infrastructure availability, market cycles, and even investor sentiment. However, the biggest percentage gains typically occur when land is first identified and shifted from raw rural into the “future urban” category, particularly if it falls within an active structure plan. A second inflection point often arrives when services such as water, stormwater and sewer are physically delivered to the site and titles become imminent.

The servicing step can act as a margin bottleneck, since infrastructure costs - especially in areas with complex topography or utility constraints can erode profits. Still, the final uplift after servicing depends heavily on the achievable lot count, the likely dwelling density, and market appetite for new housing supply.

For developers and landbankers alike, there are some crucial strategic takeaways. Most of the capital gain in land development is created before the first house is ever built. It is during these early stages especially zoning, private plan changes, and structuring consent strategies, that some of the highest dollar gains per square metre occur. Buyers in the development chain place a premium on certainty, so the fewer assumptions and constraints a future developer or builder has to deal with, the more they are willing to pay.

Ultimately, success in development isn't just about picking the right suburb or region. It’s about identifying where a site currently sits along the value chain, understanding what regulatory or physical steps are left to unlock, and then moving swiftly and strategically to capture the next tier of uplift.