Fitzgerald Road, Drury

4 Hectare live-zoned residential site

5/8/2024

This site sold for $13,850,000 +GST in 2023. It is 4 hectares (40008m2) of zoned THAB land in close proximity to Drury Station and Town Centre. This is a premium land bank development site for the following reasons:

The plan change has been complete and is zoned for terrace housing allowing for high density residential.

A fairly flat site which will support the higher density residential and minimise design difficulties with re-contouring, earthworks and stormwater. We did some very quick preliminary stormwater design on this block with minor adjustments to the EGL to find a drainage solution. It did not present major challenges.

Minimal flood plain or flood prone areas or streams contributing to building setbacks. Many development sites throughout the area have land loss due to catchment/hydrology factors.

Limited loss of “Net Developable Area” makes this an efficient site for development purposes.

Services at the gate. This is a serviced greenfields site with a 500GRP wastewater and a 450PE water supply on Fitzgerald Rd. The site sits outside the nearby designated gas line through the area. Subject to consents, this site is shovel ready. Unlike many of the other sites throughout the surrounding area that are Future Urban or even zoned land, you will not have to wait for unknown periods for infrastructure to be funded/built. This significantly increases the value of this site.

Surrounding developments are underway. This property is wedged between the Kiwi Property Drury Centre and the Fulton Hogan Drury East Precinct. There is no question of development momentum in this area or having to wait for areas to be developed, as is the case with large swathes of land in the Drury-Opaheke Plan. The risk of Government rule changes of scaling back on greenfields development in this area would be negligible.

The site has good road frontage, access and visibility for vehicles turning onto Fitzgerald Rd. Fitzgerald Rd is an existing collector road, which is also a planned future local bus route connecting to the wider network.

The site is adjacent to mixed use and varying business zones which in the future will offer excellent amenity. The site is within walkable distance to the Drury Station and town centre. The site will have good future connectivity and proximity to motorway interchanges.

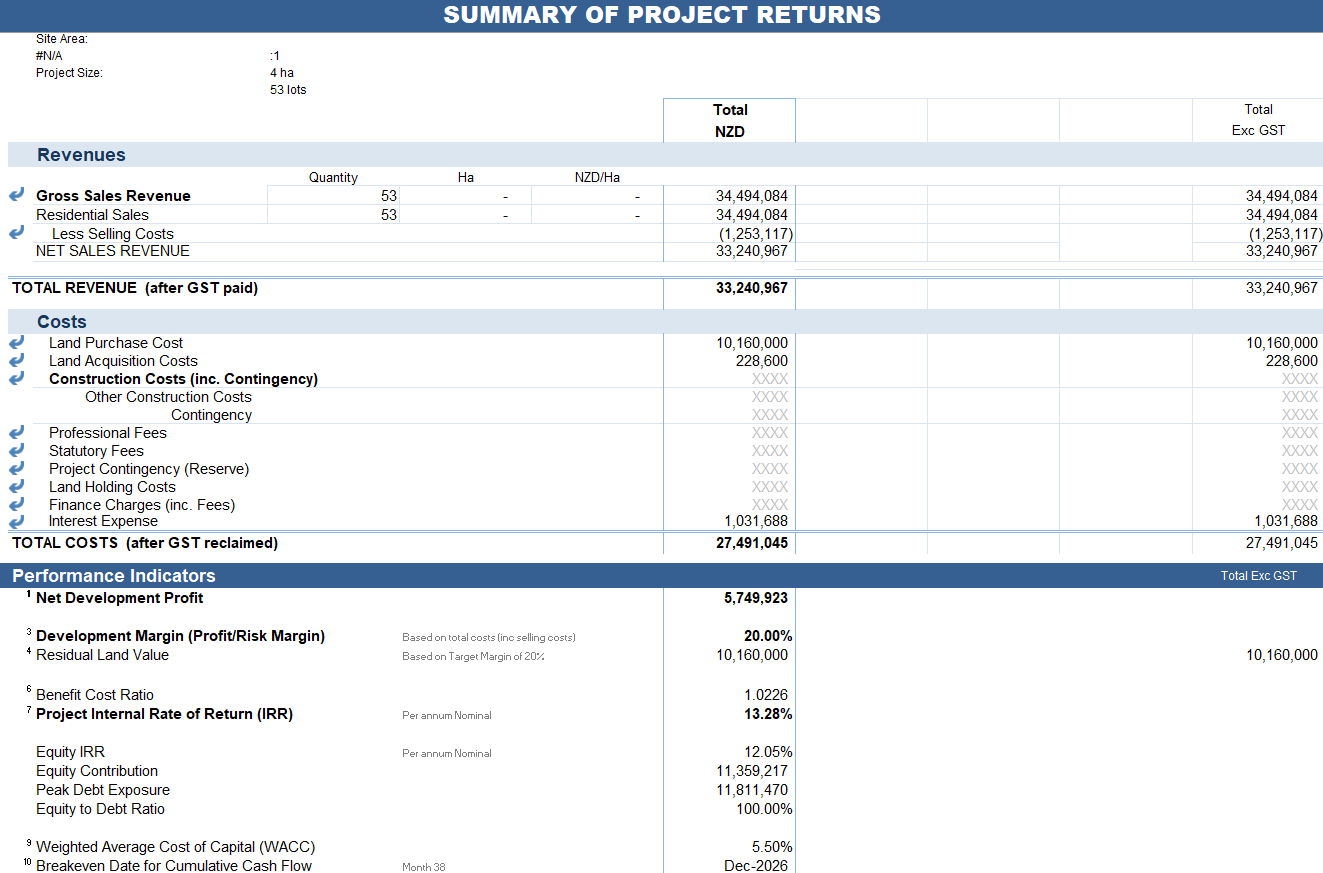

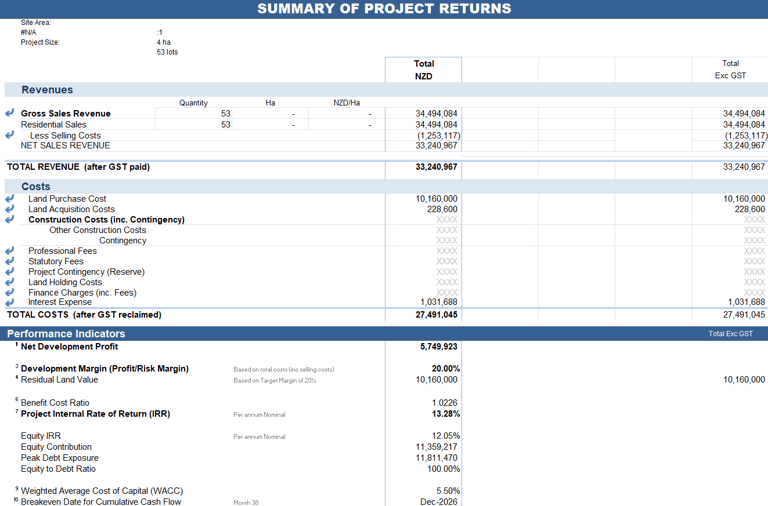

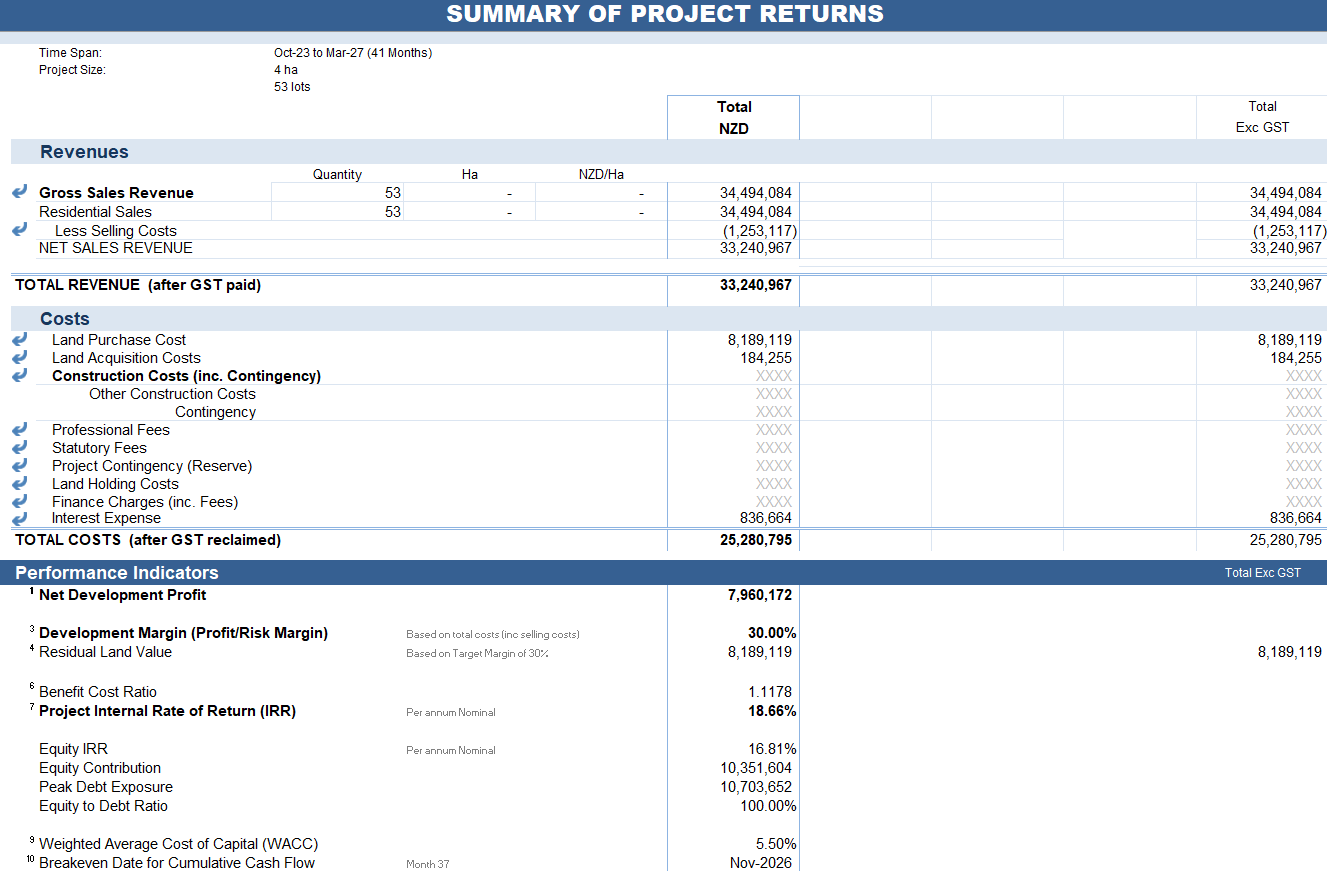

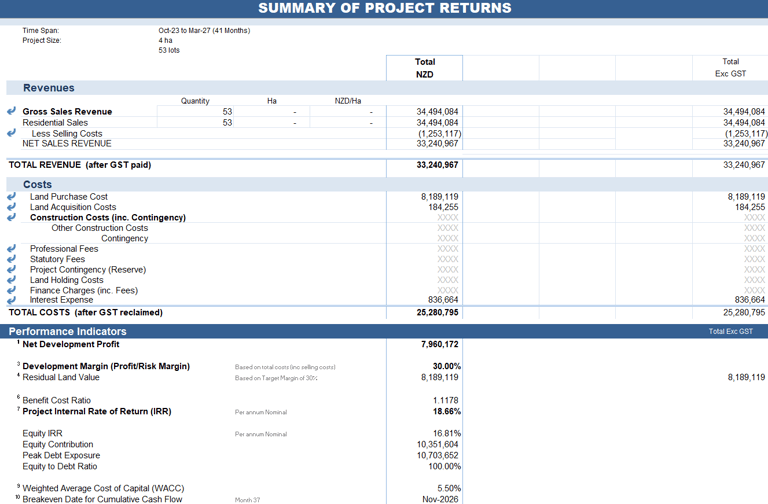

Based on these and other assessment criteria, we rated this site with a Development Index of 88%. The net developable area was assessed as 39,300m2. Loss of additional land through provision of access roads would result in a conservative net site yield of 53 lots, subject to layout constraints. This is a similar density to the Fulton Hogan Stage 1 plans next door. It is possible that this site could support significantly more lots by reducing site sizes in line with similar development densities in Drury. Based on a higher density mix of terrace housing and duplexes the net site yield of 137 lots on average lot sizes of 200m2 was assessed. EstateMaster Analysis has been completed based on these two scenarios, to calculate residual land value of this site.

Residual Land Value - Scenario 1

Some key assumptions for the conservative Scenario 1 development of 53 lots are as follows:

Average efficiency road layouts and limited loss of land to reserve

Larger average lot sizes of 500m2

Section sales only, no houses to be developed

Pre-construction period of 12 months

Construction period of 12 months

Sales period of 18 months with build up pre-sales period

Average lot sale of $700k inc GST

50% of project costs financed at 11% +fees. 50% financed through equity contribution.

As there is no approved engineering plans to schedule costs, civil construction costs based on typical rates per lot for a flat mid-sized subdivision.

Development contributions in line with current 2024 rates

All revenues and costs escalated at 2.5%

Target development margin of 30%

The outputs for this indicated a residual land value of $8,189,119+GST with a project Internal Rate of Return of 18.66% and total project costs of $25,280,000. This is an estimate for residual land value based on developing similar to that proposed in the Fulton Hogan plan.

Given the current market fundamentals, target development margins of 20% were also assessed. The outputs for this indicated a residual land value of $10,160,000+GST with a project Internal Rate of Return of 13.28% on total project costs of $27,491,045

Residual Land Value - Scenario 2

Some key assumptions for the conservative Scenario 2 development of 137 lots are as follows:

High efficiency road layouts with minimal loss of land to reserve

Average lot sizes of 200m2

Houses to be developed, consisting of a mix of terraced housing and duplexes

Pre-construction period of 16 months

Construction period of 22 months

Sales period of 24 months, including pre-sales period of 6 months

Average lot sale of $850k inc GST

50% of project costs financed at 11% +fees. 50% financed through equity contribution.

As there is no approved engineering plans to schedule costs, civil construction costs based on typical rates per lot for a flat mid-sized subdivision.

Residential construction costs based on typical unit rates for low spec two level terrace houses/duplexes. Efficiency savings applied due to scale.

Development contributions in line with current 2024 rates

All revenues and costs escalated at 2.5%

Target development margin of 30%

The outputs for this indicated a residual land value of $1,560,450+GST to maintain the target 30% development margin, which is clearly not a realistic land purchase price. The higher density option is not feasible at this margin. Depending on future outlook, some Developers may explore the higher density option further but some adjustments to expected margins would need to be made to get closer to realistic land purchase prices.

The Analysis for this piece of land would suggest that for Developers, the value of this piece of land based on discounted cash flow analysis is $8.2 – 10.2M +GST, based on a lower density project selling off bare lots. This is based on revenue and cost assumptions as at July 2024, nearly a year since this purchase went through. In this time, the market has deteriorated somewhat, however there is still a significant difference in purchase price and estimated value today. It’s unclear what is planned for this piece of land in the future but there remains no doubt that it is a good site to work with. There are a lack of good sites in Drury that tick all the boxes from an engineering perspective to support viable projects and most of these sites are sold off-market before the public get access to them.

Our gut feel is that if brought to the market today, it is a $10-12 million property to hold and develop when market fundamentals improve and the case for high density residential construction of ~150 lots becomes feasible. Often a premium has to be paid to secure the best sites. How far above what a discounted cash flow tells you to pay is a question for market outlook which further sensitivity analysis could assist with. If you believed the market will significantly rebound in the next two to three years, then this would alter many of the assumptions used in the model. How far the Vendor will move on their price expectations is also another factor. You won’t secure a property until the Vendor is satisfied but many landowners are completely clueless to the business case for how property development works. They will be comparing on a $/m2 to other sites in the area which is a flawed analysis and doesn’t show you the full picture. How far you erode away your development margin to secure the property in the hope of future property price increases within the sales period of 2-3 years away is difficult to speculate on. It is likely that this on-market site attracted significant interest and as a result a premium price was paid for this block. We suspect by a speculative Investor or perhaps a Developer currently in a favourable cash position.